Originally published by Jonathan Shapiro, Australian Financial Review on 23 January 2022

A rise in petrol prices and housing costs is forecast to lift the Reserve Bank of Australia’s preferred measure of inflation to its highest level in more than seven years this week, compelling the central bank to ditch its $350 billion bond buying program and potentially raise the cash rate before the end of the year.

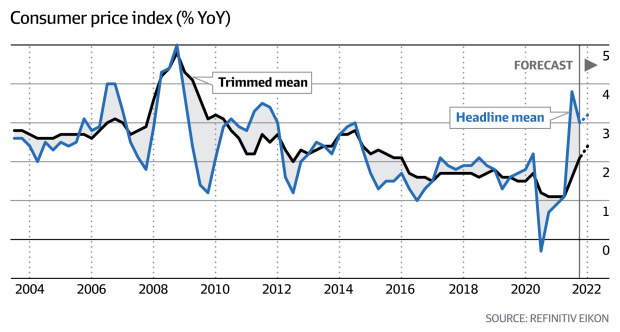

Economists expect trimmed mean inflation, or “core inflation”, to have increased by 0.7 percentage points in the three months to December 31, at an annual rate of 2.4 per cent when official statistics are released on Tuesday.

That is above the Reserve Bank’s November forecast of a 2.25 per cent annualised rate and will raise further questions about the central bank’s commitment to maintain its ultra-low cash rate in the face of rising inflation.

The central bank is already widely tipped to wind down its $350 billion government bond buying program this year and relay the decision at its board meeting on February 1.

But governor Philip Lowe has repeatedly pushed back on bond market pricing that has suggested multiple cash hikes by the end of the year, stating that wages growth would have to lift to 3 per cent for rate increase conditions to be met.

A 7 per cent increase in fuel prices over the December quarter, a 3 per cent rise in housing related costs, higher clothing and footwear prices and weather-related increases in food prices have led economists to forecast Tuesday’s headline Consumer Price Index to increase at 3.1 per cent annually.

Core inflation, the trimmed mean Consumer Price Index rate, is forecast to increase by 2.4 per cent annually, a level not reached since the September 2014 quarter.

“The risk is skewed to the upside amid a strong activity quarter post lockdown,” RBC Capital Markets economists told clients on Friday.

The key data release comes a day ahead of the Australia Day holiday and in a week when the United States Federal Reserve’s Open Markets Committee meets over two days.

As inflation rates are rising globally, more central banks are being forced to tighten conditions by signalling an end to bond purchase programs, or quantitative easing, and bringing forward expected interest rate increases.

The Reserve Bank is widely tipped to reveal that it will wind down its $350 billion QE program when its board meets in February amid a decline in the jobless rate.

“Given how the labour market finished 2021, an explicit decision to move to quantitative tightening is likely on the table for the February meeting,” ANZ economists told clients on Friday,

“The Q4 CPI report in the week ahead may be enough to seal it.”

Omicron Hit Temporary

A strong economic recovery has been derailed to some extent by an Omicron induced decline in activity. But economists are betting that the slowdown will be temporary while supply chain related disruptions will exacerbate supply chain pressure.

ANZ economists say an increase in the core inflation rate above the 3 per cent upper range of the RBA target was not their central base. But it was forecasting that the measure will hit or exceed the mid-point of its 2 to 3 per cent target for three consecutive quarters.

“While we think the RBA will continue to emphasise patience, its forward guidance on interest rates will need to shift,” the ANZ economists told clients.

“A lift-off in 2023 will likely become its central case, with 2022 no longer ruled out – which will represent a big shift given how strongly Governor Lowe has pushed back against market pricing of a move this year.”

Westpac’s economists led by Bill Evans forecast that the Reserve Bank will eat its words and raise the cash rate in August from 0.1 per cent, rising to 0.5 per cent by the end of the year.

While that prediction is bold relative to other forecasters, bond market contracts are implying a hike to 0.5 per cent by August and 1 per cent by December.

xcvgv

This document has been provided to you for your general information and does not take into account your objectives, financial situation and needs and must not be relied upon by you as personal financial product advice that has been provided to you by iInvest. If you require advice regarding any aspect of the information and statements of opinion set out in this document, particularly as to whether you should base an investment decision upon the information or statements of opinion set out in this document, please contact your financial adviser.

Distribution

The material contained in this communication is prepared for the exclusive use of clients of iInvest. iInvest is an Authorised Representative (#431611) of Zodiac Securities Pty Ltd (ABN 76142982554) (AFSL #398350).

The information contained herein is confidential and may be legally privileged. If you are not the intended recipient, confidentiality is not lost nor privilege waived by your receipt of it. Please delete and destroy all copies. You should not use, copy, disclose or distribute this information without the express written authority of iInvest.

Disclaimer & Disclosure

iInvest, its related companies, officers, employees and agents may have a relevant interest in some of the securities mentioned but those holdings are not material unless disclosed in this communication. These holdings (or absence of holdings) may change at any time after publication of this communication, without notice.

iInvest, its related companies, officers, employees and agents may earn income, fees, brokerage or commissions or other benefits as a result of recommendations, dealing or transactions in the securities mentioned in this communication. These interests do not influence iInvest in giving the general advice contained in this communication. iInvest, its related companies, officers, employees and agents may trade in financial products which is contrary to the recommendations given in this communication.

You should not act on any recommendation made in this document without first consulting your investment adviser in order to ascertain whether the recommendation (if any) is appropriate, having regard to your investment objectives, financial situation and particular needs. Nothing in this communication shall be construed as a solicitation to buy or sell a financial product, or to engage in or refrain from engaging in any transaction. We cannot guarantee that the integrity of this communication has been maintained, is free from errors, omissions, misstatements, virus interception or interference.

Copyright © iInvest Securities, All rights reserved.